Top 7 Home Loan Mistakes to Avoid Before Applying

Applying for a home loan can be a daunting process, especially for first-time homebuyers. To ensure a smoother experience, it's vital to avoid common mistakes that can lead to complications down the road. One of the biggest mistakes is neglecting to check your credit score before applying. A low credit score can result in higher interest rates or even loan denial. Consumer Financial Protection Bureau recommends reviewing your credit report and addressing any discrepancies to improve your chances of securing a favorable loan.

Another common pitfall is failing to understand the total costs associated with taking out a home loan. Many borrowers focus solely on the monthly payment and interest rate, overlooking additional expenses such as closing costs, property taxes, and homeowners insurance. It’s crucial to create a comprehensive budget that includes these costs. Additionally, speaking with a reputable mortgage advisor can provide clarity on what to expect. For more insights on managing home loan expenses, visit NAHREP.

Essential Tips for Securing the Best Mortgage Rate

Securing the best mortgage rate is crucial for homeowners, as even a slight difference can save thousands of dollars over the life of the loan. Here are some essential tips to help you get the most favorable terms:

- Improve Your Credit Score: A higher credit score generally leads to better mortgage rates. Consider checking your credit report for any errors and work on paying down existing debts.

- Shop Around: Do not settle for the first offer you receive. Rates can vary significantly among lenders. Utilize online resources, like Bankrate, to compare mortgage rates.

Additionally, timing can play a crucial role in securing a competitive mortgage rate. Market conditions fluctuate, impacting rates. Consider locking in a rate when they are low. It's also beneficial to come prepared with a substantial down payment, as larger payments can sometimes lead to better rates. Lastly, working with a knowledgeable mortgage broker can offer insights and access to rates that aren’t publicly advertised.

“The biggest long-term mistake you can make with your mortgage is settling for a high interest rate.”

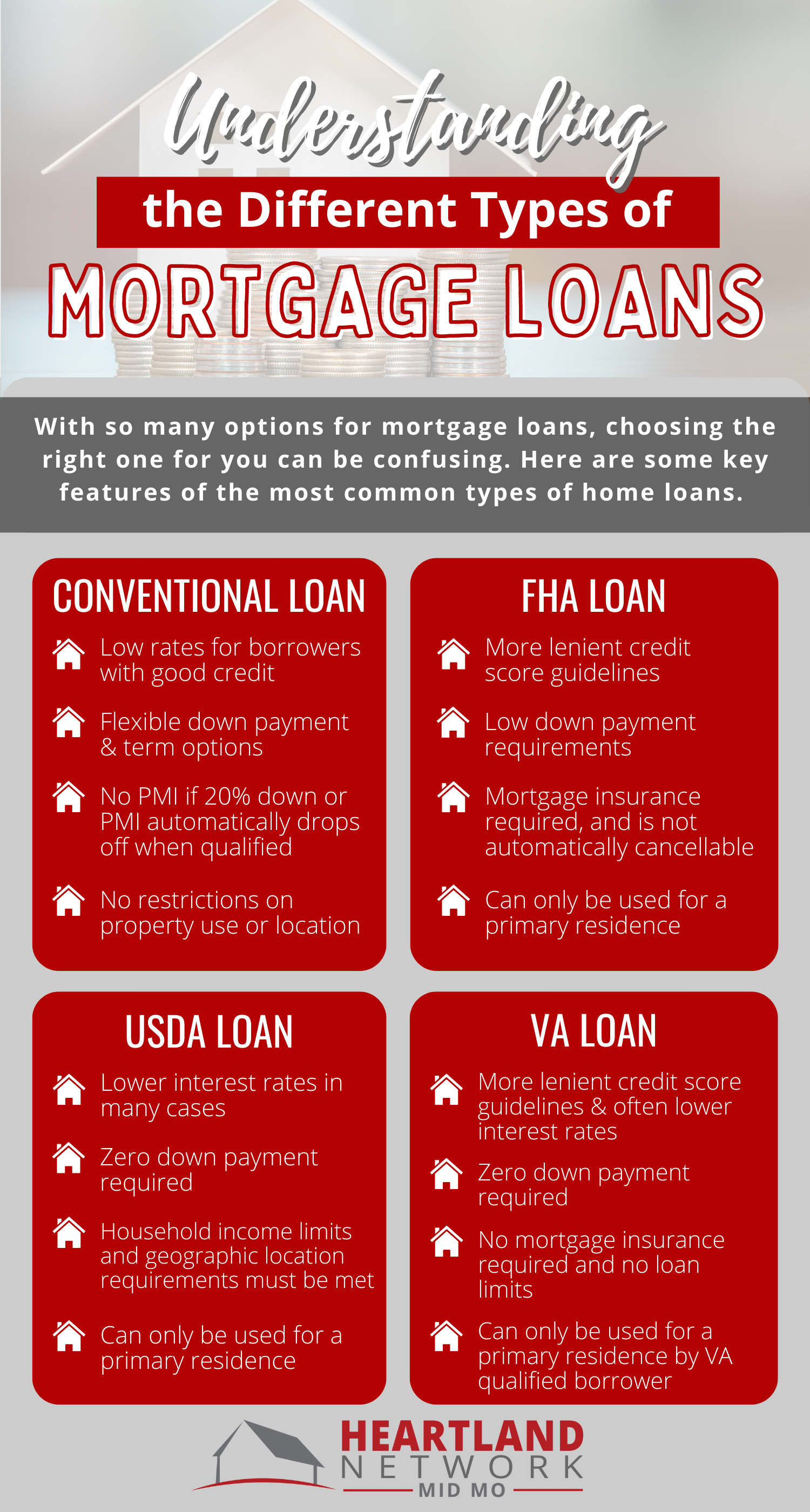

What Homebuyers Need to Know About Loan Types and Eligibility

When navigating the complex world of home buying, understanding the different loan types is essential. Each type comes with its own advantages and considerations. The most common options include conventional loans, which require higher credit scores and interest rates reflecting market conditions, and FHA loans, backed by the Federal Housing Administration, designed for low-to-moderate-income borrowers with lower credit eligibility. Moreover, VA loans are a great option for veterans and active military personnel, offering favorable terms without the need for down payments.

Aside from knowing loan types, potential homebuyers must also be aware of the eligibility criteria set by lenders. Key factors typically include credit score, debt-to-income ratio, and employment history. A good credit score can significantly improve loan terms, while a lower debt-to-income ratio demonstrates financial stability. To give you a clearer idea, here are some eligibility requirements for various loans:

- Conventional loans: Minimum credit score of around 620.

- FHA loans: Accepting scores as low as 580 for 3.5% down payment.

- VA loans: No official minimum score, but lenders prefer at least 620.